Homeowners Insurance Cost – Factors That Affect Your Rates

Homeowners insurance provides crucial protection from damage to both their homes and property, but its cost varies widely depending on factors like its location, age and construction materials as well as factors like credit history and prior claim histories.

Understanding what factors contribute to homeowner insurance costs can assist consumers and real estate agents alike in comparing quotes and finding an optimal policy within their budget.

Premiums

General, homes in the New York City area tend to have higher premiums; however, this varies by city depending on factors like weather patterns, household values and construction costs. Below is a table which lists average annual premiums for policies offering various levels of dwelling coverage (the part of an insurance policy which protects your house’s structure).

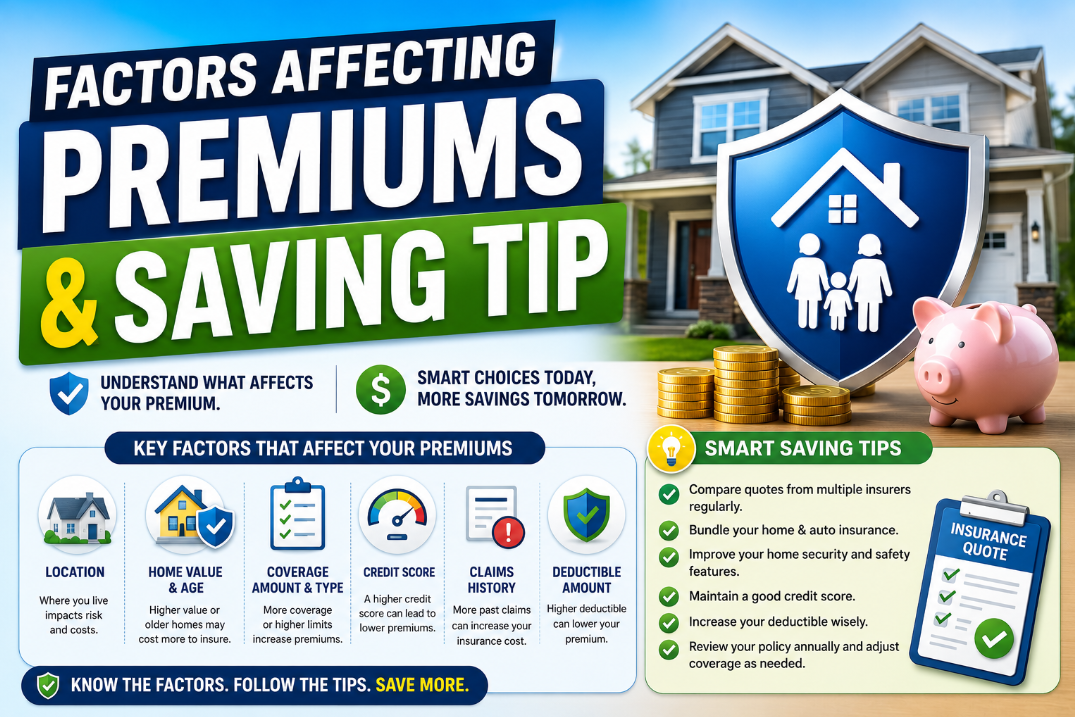

Insurers also consider the age and renovations made to your home when making a determination on its insurance cost. Older homes may cost more due to not meeting modern safety standards and being constructed from materials more susceptible to fire damage or storm-induced storm damage; newer properties tend to be cheaper to insure.

Some states have laws that limit how much insurers can charge for homeowners insurance policies, while other allow individual insurance providers to set their own prices, which may differ significantly.

Home insurance premiums often depend on two key variables: choosing an appropriate deductible amount and whether or not any claims have been filed in the past. A higher deductible typically lowers premiums; filing claims could raise them.

Many homeowners insurance providers use credit-based scores to determine your rate and premium costs; improving your score could have a considerable effect on how much home insurance premiums cost over time. Building your credit can help lower premiums in the long run.

Your premium will also depend on factors like its location, construction materials and size; state regulations regarding risk exposure (such as hurricanes), as well as weather events that increase rates such as hurricanes or extreme storms that affect coastal regions.

Some states mandate residents purchase additional coverage, like flood or earthquake insurance, which can add significantly to your homeowners insurance costs. If you live in an area prone to natural disasters, exploring private market options and looking for competitive home insurance rates might also help save on homeowners insurance premiums. Furthermore, taking steps such as upgrading to an earthquake- or flooding-resistant roof might reduce premiums further.

Deductibles

A deductible is the amount you are responsible for paying out-of-pocket before an insurer begins paying on a claim, and is an important component of homeowners insurance policies as it helps keep premiums affordable. A higher deductible could decrease premium costs; just be sure that you can cover it if a claim occurs!

Homeowners insurance rates differ by state, with certain areas costing significantly more than others due to weather patterns influencing base rates. For instance, insuring homes in tornado-prone or hurricane-prone coastal regions will cost significantly more than similar properties insured elsewhere with less weather-related risks.

Other factors affecting home insurance costs besides location include age and condition of your home, deductible/coverage limits, optional policy add-ons, credit history (in most states) as well as your location. It’s best to shop around each year as this gives you the best chance at securing an affordable policy price.

Your premium could increase if you have filed any home insurance claims in the past, as claims raise your risk profile and cause insurers to charge more for home coverage.

Homeowners insurance premiums have also seen increases across many states due to an increase in natural disasters and other hazards, like storm surges. Last year alone there were 27 disasters with damages exceeding $1 billion each; that number represents more than double what had occurred on average over 10 years prior. Insurance companies often need reinsurance policies in order to cover high payouts resulting from catastrophic events; as a result, these higher costs are passed along through higher premiums paid by homeowners.

Some strategies for lowering home insurance costs include bundling your auto and homeowners policies together and adjusting or increasing coverage limits accordingly. You could also save by installing home safety features like burglar alarms or smart water leak sensors; paying upfront rather than making monthly payments via an escrow account attached to your mortgage; and joining rewards programs offered by insurers.

Coverages

Homeowners insurance provides protection from property damage caused by fire, smoke, burglary and other events, including repair or reconstruction costs if your home is damaged as a result of one. Your amount of coverage depends on its value as well as any risk factors in your area; homes located near tornado-prone regions require greater dwelling coverage than those in low risk states with no likelihood of these storms.

Other variables that could effected homeowners insurance costs include factors like size and age of your home, proximity to fire stations and presence or absence of pools or trampolines – these all may increase rates due to being high risk for injury. Security systems and certain safety features, like burglar alarm systems can either lower or raise premiums; similarly trampolines and swimming pools could make things even more costly due to being high risk.

Your state and city also play a role in the cost of homeowners insurance. New York stands out as being among the more costly places for home insurance premiums; yet its average premium remains lower than its national counterpart due to high home values and construction costs in New York state.

Hover over your state on the map to get an idea of average homeowners insurance costs in your region. Homeowners insurance costs tend to be highest in states at high risk for natural disasters like wildfires and hurricanes; insurers tend to charge higher premiums as more claims need to be paid out in these situations.

Some states, like New York, don’t permit insurers to use credit scores when setting home insurance rates; but in Texas and Florida your credit can have an enormous impact on premiums; it is therefore imperative that you work on improving it before shopping for home insurance as this will save you money in the long run.

Saving tip

Factors that influence homeowners insurance costs may be out of your hands; however, by reducing risk through home improvements and other preventive measures you can help to make premiums more manageable over time.

Renovations that make your house less vulnerable to damage may qualify you for discounts, while adding smoke detectors, burglar alarms, or interior sprinkler systems may help decrease rates as well. When considering large scale changes be sure to consult with an agent as they can assess how these changes impact homeowners insurance costs over time and make recommendations to minimize them further.

Some states have regulations governing how much insurers can increase rates after weather- or catastrophe losses, in order to strike a balance between affordability and fairness for policyholders. By becoming acquainted with these limits, you can respond confidently when facing surcharges if they seem excessive; conversely having an excellent credit history can significantly lower homeowners insurance premiums; insurers use your score as an indicator of likelihood that claims will be filed; having one will lead to reduced premiums over time.